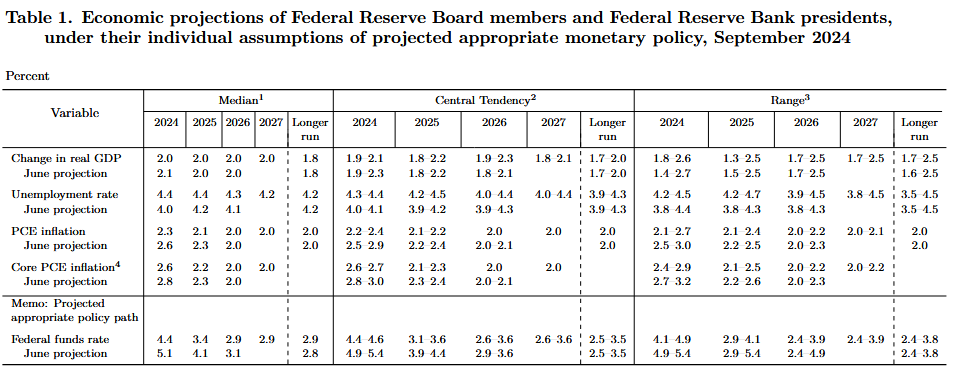

Dubai,UAE,Oct 18,2024-The Federal Reserve (FED) has begun its rate-cutting cycle with a 50-basis-point cut in the September meeting, similar to the first cut in 2007. This significant reduction was prompted by the recent spike in the unemployment rate. In June, the Federal Reserve projected that unemployment would be 4% by the end of the year, but just two months later, it has already reached 4.3%. Historically, when unemployment rises this quickly, the trend often continues for several months.

The FED’s latest forecast projects unemployment at 4.4% for both 2024 and 2025, suggesting that officials do not expect further increases beyond the coming months—a prediction that diverges from historical patterns. However, the first two data points after unemployment reached 4.3% have been more optimistic than expected, with the rate falling to 4.1%. In this article, FTD Limited shares insights on where the economy is headed, whether the FED will need to continue cutting rates, and if a soft landing is still possible.

(FOMC Projections)

©Federal Reserve Bank

Aside from the unemployment rate, the Federal Reserve also lowered its inflation and federal funds rate projections at the September meeting. Both PCE and core PCE inflation were revised down for 2024 and 2025, with the inflation target expected to be reached by early 2026, according to projections. Despite the downward revision in inflation and the upward revision in unemployment, GDP estimates remain steady at 2% for 2025, 2026, and 2027.

The FED also raised its long-term federal funds rate target to 2.9% from 2.8%, indicating that members believe the neutral rate has edged slightly higher since June.

In light of the significant upward revision in unemployment and the faster-than-expected decline in inflation, the Federal Reserve opted for a larger, 50-basis-point rate cut. This likely serves as a preemptive move to balance inflation and unemployment, as sudden increases in unemployment often signal more economic difficulties ahead.

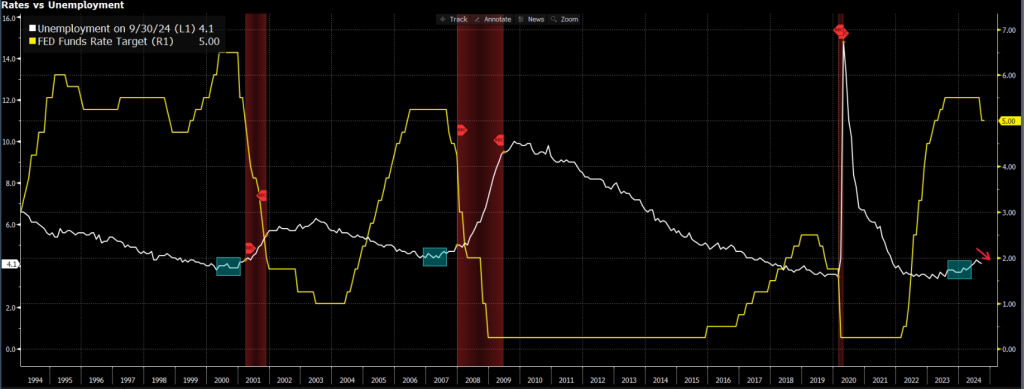

(Rates vs Unemployment – US Recessions)

©Bloomberg

Historically, when unemployment rises quickly, it tends to continue spiraling out of control, often resulting in a recession and aggressive rate cuts. Economist Claudia Sahm developed a rule to identify this pattern, known as the Sahm Rule. According to the rule, when the three-month average of unemployment increases by 0.5 percentage points above its 12-month low, the Sahm Rule is triggered. This rule has been about 85% accurate since 1950 and was triggered again this year when unemployment reached 4.3%, though just barely.

Since then, two jobs reports have shown strong results, each reducing the unemployment rate by 0.1%. In the latest report, nonfarm payrolls rose by 254k, supported by rising full-time employment and strong private-sector growth.

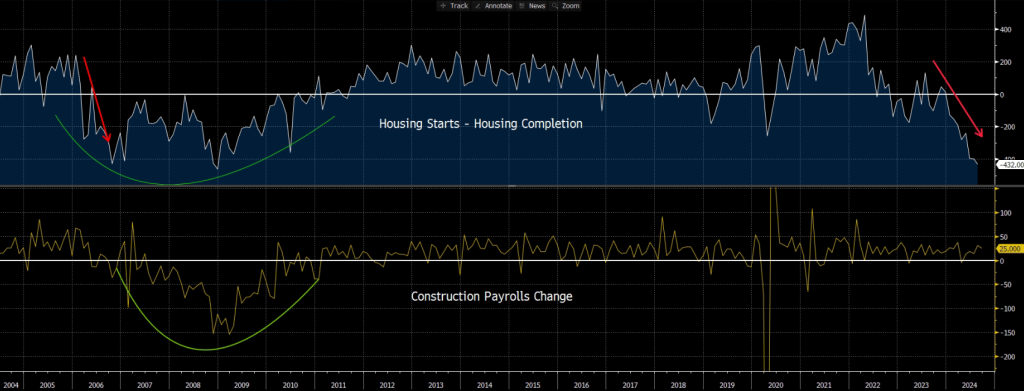

(Housing Starts and Completions Spread vs Construction Sector Payrolls Change)

©Bloomberg

If we take a closer look at the economy, there are both positives and negatives at play. One red flag is emerging from the construction sector. The spread between housing starts and housing completions has fallen into negative territory and has remained there since the start of the year. This indicates that active construction projects are steadily declining. Despite this, construction payrolls have continued to rise.

A similar, though not identical, situation occurred in 2006, just before the 2008 recession. When the spread between housing starts and completions stayed below zero for 12 months, construction jobs began to decline as well. During the 2008 crisis, amplified by other factors, construction jobs fell sharply for over two years.

Currently, the spread between housing starts and completions is declining even faster than it did in 2006 and has been below zero for eight months. If the same lagging effect occurs, it could push the unemployment rate higher in the coming months or even years. Mortgage rates remain elevated, but if the FED’s recent rate cut helps to reignite the housing market, the damage may be less severe than during the 2008 crisis. However, this could be a subtle but important factor to monitor for a potential hard-landing scenario.

(Savings Rate – Credit Card Debt)

©Bloomberg

Another red flag comes from the savings rate. Despite high inflation and interest rates, consumer spending in the U.S. has remained strong, which has helped the economy fare better than most economists predicted. One reason consumption has stayed high for so long is the extra savings accumulated during the COVID-19 shock, whether from stimulus packages or reduced spending. While the savings rate fluctuated during that time, total savings increased significantly to historically high levels.

Since the “back to normal” period, households have been tapping into these savings to fuel spending. Household income has been rising more slowly than spending for several months now, and while this has kept the economy strong, it won’t last forever. From 2013 to 2020, the average savings rate was 5.9%. However, since 2023, the average savings rate has dropped to 4.8%, an 18% decline. If unemployment or inflation doesn’t spike again, these lower savings levels may not pose a significant problem. But if a new shock occurs—such as a recession with rising unemployment or steadily increasing inflation—low savings could amplify the impact.

When examining savings, it’s also important to consider debt levels. U.S. household credit card debt has risen significantly since 2021. There are two factors to consider regarding this increase. First, post-COVID, the already growing trend of online shopping reached new heights, potentially contributing to the rise in debt. Second, inflation makes the increase in debt appear larger than the real value. However, the upward trend in debt is undeniably steep and should be closely monitored in the coming quarters, alongside the savings rate.

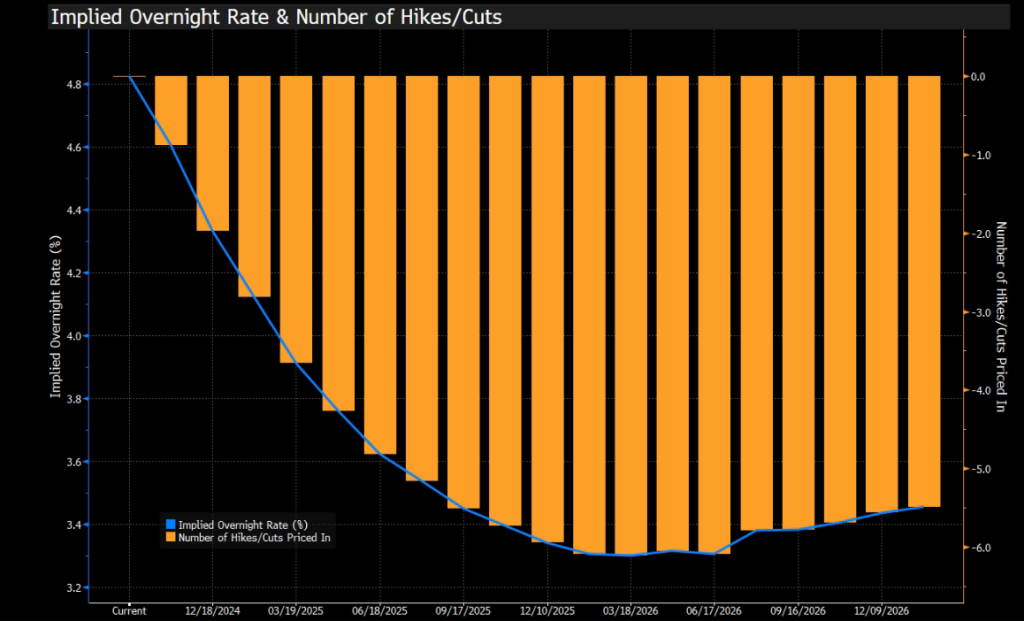

(Implied Federal Funds Rate)

©Bloomberg

Burc Oran, Senior Market Research Specialist at FTD Limited, commented:

“Although there are some serious red flags, the U.S. economy is performing much better than many forecasters predicted. With inflation falling and the FED beginning to cut rates, consumers may continue spending as long as there isn’t a significant spike in unemployment. Growth will likely moderate further in the coming quarters, but if the U.S. economy can remain strong enough to avoid a recession in the next three quarters, a soft landing is likely to be achieved, considering the rate cuts and a stabilizing manufacturing sector. So far, the services sector has been keeping the economy strong, but for balance to be restored, manufacturing demand must also increase alongside services.”

Markets expect the FED to lower the federal funds rate to 3.5% by the end of 2025, implying six 25-basis-point cuts, including the two cuts anticipated this year. This scenario appears rational, given the risks and the economy’s strong points. However, if unemployment rises sharply and the low savings rate can no longer compensate for the income shortfall, the likelihood of a hard landing will increase significantly, potentially leading to more aggressive rate cuts, bringing rates below the projected 3.5%.

The chance of a hard landing isn’t too high right now, despite the risks mentioned, as the U.S. economy—and particularly the job market—remains strong. According to the latest surveys, economists see a 30% chance of recession in the next 12 months. However, traders should pay close attention to savings rates, household debt, and unemployment simultaneously to manage risk in case a recession materializes.

About FTD Limited

FTD Limited, a multi-asset brokerage firm established in 2017, offers a trading platform with access to various asset classes (FX, equities, futures, indices) on major global exchanges. Their technology prioritizes fast and efficient execution, clearing, and liquidity solutions. They cater to institutional investors, high net worth individuals, and professional clients with a global presence in the Middle East and Asia.

For more information, please visit www.ftdsystem.com or contact marketing@ftdsystem.com

Name: Burc Oran

Company name: FTD Limited

Email: marketing@ftdsystem.com

Location: Dubai, UAE